មគ្គុទ្ទេសក៍ជួញដូរ

How to Choose a Forex Broker: 2026 Checklist for Traders

A practical 2026 checklist for choosing a forex broker — regulation, spreads, execution, platform tools, and withdrawal terms. No fluff, no hype.

Picking the wrong broker costs you in ways that never show up on a P&L — slippage on news, withdrawal delays, fine print on leverage. This 2026 checklist walks through the eight criteria that separate a professional trading environment from a headache, so you know exactly what to look for in a broker before you fund an account.

Regulation: The Only Non-Negotiable Filter

Before you compare spreads, platforms, or leverage tiers, check the license. A broker's regulator determines whether your funds survive if the firm goes under — and whether you have a credible avenue for dispute resolution when something goes wrong. Everything else is negotiable. Regulation is not.

What Tier-1 Regulation Actually Means

Tier-1 regulators enforce strict capital adequacy rules, mandatory client fund segregation, and regular reporting. They also require negative balance protection — meaning you can never lose more than your account balance, even in extreme market gaps. If a broker fails while holding your money, tier-1 regimes typically ring-fence client deposits from the firm's operating capital, giving you a strong claim to full recovery.

The Major Regulators and What They Require

Regulator Jurisdiction Key Requirements FCA UK £1M minimum capital; client money must be held in segregated accounts; FSCS protects up to £85,000 per client if the firm fails; mandatory negative balance protection CySEC Cyprus (EU) €730K minimum capital; ICF compensation up to €20,000; ESMA-compliant leverage caps (30:1 for major forex); negative balance protection required ASIC Australia A$1M net tangible assets; client money must be held in a statutory trust account; leverage capped at 30:1 for retail clients; mandatory negative balance protection MAS Singapore S$1M base capital; strict segregation rules; leverage capped at 20:1 for retail; regular audited financial reporting CFTC / NFA USA Minimum net capital of $20M; mandatory segregation of retail funds; FIFO rule for position management; no hedging allowed; leverage typically 50:1 on major pairs

License Numbers vs. Active Oversight

A broker can display a license number on its website without being under active supervision. Some firms register in one jurisdiction and operate from another with no real compliance. Always verify on the regulator's own register: the FCA's Financial Services Register, CySEC's online registry, ASIC's Professional Registers, or the NFA's BASIC database. Check that the license is current and that the entity name matches exactly. A mismatch of even one word can signal a cloned firm.

The Offshore Trap and What "Passporting" Means

Unregulated or "offshore" brokers — often holding a registration from Vanuatu, the Seychelles, or the British Virgin Islands — may offer high leverage and no reporting requirements, but they also offer zero client protection. If they freeze withdrawals or disappear, you have no regulator to complain to. In the EU, passporting allows a broker licensed in one member state (e.g., CySEC in Cyprus) to offer services across all EU countries without separate licenses. That is legitimate — but only if the home regulator enforces ESMA rules. A broker claiming to be "regulated in Europe" without naming a specific competent authority is a red flag.

A regulated broker cannot prevent losses. But it can ensure that when a trade goes wrong, your loss stops at your account balance — and that your money is not treated as the firm's working capital.

Spreads, Commissions, and the Real Cost of a Trade

The spread between the bid and ask price is the most visible cost you pay per trade, but it is rarely the only one. Understanding how raw spreads, commissions, and hidden fees stack up determines whether your strategy survives after costs.

Raw Spreads vs. Fixed Spreads

Raw spreads are the interbank market spread — the actual distance between bid and ask before the broker adds any markup. They fluctuate with liquidity, compressing to 0.1–0.3 pips on EUR/USD, GBP/USD, and USD/JPY during peak London and New York overlap, and widening during low-liquidity hours like Friday close or Asian session lulls.

Fixed spreads are set by the broker regardless of market conditions. They offer predictability — useful during news events when raw spreads can spike to 2–3 pips — but the fixed number is almost always wider than the average raw spread in liquid conditions. A fixed 1.2-pip EUR/USD spread costs more than a raw 0.2-pip spread 90% of the time.

Commission Models: Per-Lot Flat Fee vs. Spread-Only

Brokers typically use one of two structures:

Spread-only (dealing desk / market maker): No separate commission. The broker's revenue comes entirely from the spread, which is marked up above the raw rate. A 1.0-pip EUR/USD spread with no commission is effectively a 1.0-pip cost per side.

Raw spread + commission (ECN/STP): The broker passes the raw spread through and charges a flat fee per lot. Typical rates: $3.50 per side per standard lot (100k units), or $7 round-turn.

Worked example — all-in cost per round turn (one buy + one sell) on EUR/USD:

ModelSpread per sideCommissionTotal cost per round turn (1 lot) Raw + commission0.2 pips$7 round-turn$9 (0.4 pips × $10 per pip + $7) Spread-only1.0 pip$0$10 (1.0 pip × $10 per pip × 1 lot)

The raw-spread model saves $1 per round turn on this pair. Multiply that across 20–50 trades a day and the difference is material.

Hidden Costs That Eat Into Your Account

Swap / rollover rates: The interest differential between the two currencies in a pair, charged or credited at 5:00 PM EST daily. A swing trader holding positions for days or weeks can see swap costs outweigh entry spreads. Check whether a broker offers Islamic (swap-free) accounts if your strategy or beliefs require it.

Inactivity fees: Some brokers deduct a monthly fee after 90–180 days of no trading activity. Scalpers who trade daily rarely trigger this; longer-term position traders who log in once a week should verify the policy.

Currency conversion fees: If you deposit USD but trade a EUR-denominated account (or vice versa), the broker converts at a rate that includes a hidden markup — often 0.5%–1%. Deposit and trade in the same currency to avoid this.

Match the Cost Structure to Your Style

Scalpers and day traders should prioritize low spreads and low commissions above all else — swap rates barely matter when positions close within minutes. ECN/STP models with raw spreads and per-lot commissions are the right fit.

Swing traders and position traders should focus on swap rates and inactivity fees. A broker offering competitive rollover rates (or a swap-free account) and no inactivity fee is more important than shaving 0.1 pips off the spread on entry.

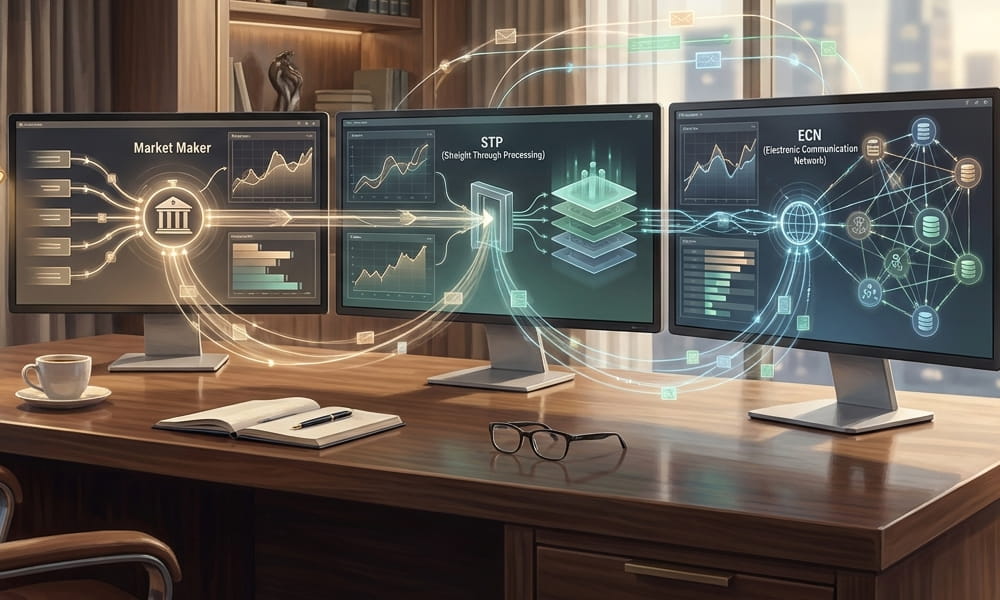

Execution Model: Market Maker, STP, or ECN?

The execution model a broker uses determines how your orders are routed, filled, and priced. It directly affects requotes, slippage, and whether your broker has a conflict of interest in your trade's outcome. There are three main models.

Market Maker (Dealing Desk)

A Market Maker creates its own liquidity pool and takes the opposite side of your trade. When you buy EUR/USD, the broker sells it to you from its own inventory. This creates a built-in conflict of interest — the broker profits when you lose money. During high-volatility events like NFP releases or central-bank rate decisions, Market Makers often widen spreads dramatically or issue requotes because their in-house dealing desk manually approves each fill. Slippage can be severe and consistently against the trader.

STP (Straight-Through Processing)

STP brokers send your orders directly to liquidity providers without dealer intervention. Orders are matched automatically, which eliminates requotes and reduces slippage. The broker earns via a markup on the spread rather than betting against you. STP is a middle ground — faster fills than a dealing desk, but spreads may still widen during news events as the underlying liquidity providers adjust their pricing.

ECN (Electronic Communication Network)

ECN brokers aggregate quotes from multiple banks and institutional liquidity providers into a central order book. Your buy and sell orders are matched anonymously against other participants. The result is the tightest raw spreads available, but the broker charges a fixed commission per lot (typically $3–$7 round-turn) instead of a spread markup. ECN execution has no dealing desk intervention, so requotes are virtually eliminated. Slippage can still occur during extreme volatility, but it is generally smaller and can work in the trader's favour.

Which Model Fits Your Trading Style?

Scalpers and day traders — ECN or STP. The speed and absence of requotes are essential for short holding times. Accept the commission as a trade-off for tighter spreads.

Swing and position traders — STP or a reputable Market Maker. Wider spreads matter less over multi-day holds, but check that the broker's execution policy explicitly states no dealing-desk intervention during news events.

New traders — STP. You avoid the conflict of interest in a Market Maker while keeping a simple cost structure (no commission calculation).

Review the broker's execution policy disclosure on their website. Look for language about order-routing logic, maximum slippage during news, and whether the broker operates a dealing desk during specific sessions. A broker that refuses to disclose its model in plain terms is a red flag.

Platforms and Tools: MT4, MT5, and Beyond

The platform is where you execute every trade, so it deserves more scrutiny than demo-account aesthetics. Here is what to check before committing live capital.

MT4 vs. MT5: Which Fits Your Style?

MetaTrader 4 (MT4) remains the standard for retail forex traders. It supports 9 timeframes, 4 pending order types, and a mature ecosystem of Expert Advisors (EAs) — automated trading scripts written in MQL4. Its backtester is single-threaded but reliable for simple strategies.

MetaTrader 5 (MT5) adds 21 timeframes, 6 pending order types, and a multi-threaded strategy tester that runs faster on modern CPUs. MT5 covers more asset classes natively — forex, stocks, futures, commodities, and indices — and includes a built-in economic calendar and depth-of-market (DOM) view. The trade-off: many third-party EAs and indicators written for MT4 do not run on MT5 without a rewrite. If you rely on a specific EA, confirm MT5 compatibility before switching.

Proprietary Platforms and Mobile Apps

A broker's web platform and mobile app matter for traders who manage positions away from the desktop. Look for one-click trading (no confirmation pop-up), advanced charting with drawing tools and at least 30 indicators, and an integrated economic calendar that shows high-impact events alongside your open trades. Execution speed on mobile should match the desktop version — test limit-order fills during high-volatility sessions before funding a live account.

Automation: EAs, APIs, and VPS

Automated traders need three things: (1) full EA support on MT4 or MT5 with no restrictions on trading frequency, (2) a documented API (REST or FIX) for custom algorithmic strategies, and (3) a low-latency Virtual Private Server (VPS) option — ideally free above a minimum account balance or monthly volume. Check whether the broker restricts EA usage during news events; some do, and that can break a scalping robot's logic.

Essential Risk and Execution Tools

A checklist of non-negotiable platform features:

Negative balance protection — ensures you never owe the broker more than your deposit. Required in some jurisdictions; verify it applies to your account type.

Guaranteed stop-loss orders (GSLOs) — fill at the exact level regardless of slippage or gapping. Usually carries a premium spread, but essential for high-impact news holds.

Depth of market (DOM) — shows real-time liquidity at each price level. Useful for traders who need to gauge order-book thickness before entering large positions.

Risk management alerts — push notifications for margin level thresholds, drawdown limits, or pending order triggers.

Stability Over Flashy Features

A platform with 100 charting tools is worthless if it disconnects during a NFP release. Check the broker's server locations — ideally within 50–100 milliseconds of your trading desk — and look for uptime guarantees in the client agreement. Independent latency tests (many are published on forex forums) give a real-world measure. Prioritise execution reliability over interface bells and whistles; you can always add third-party charting tools later.

Leverage, Margin, and Position Sizing Limits

What Leverage Actually Does to Your Capital

Leverage is a loan from the broker that multiplies your buying power. Margin is the deposit required to open and maintain a position. The ratio tells you how much capital you need per standard lot (100,000 units of base currency).

At 1:30 leverage — the ESMA cap for major currency pairs — a standard lot of EUR/USD at 1.10 requires roughly $3,667 in margin (100,000 × 1.10 ÷ 30). At 1:500 leverage, that same position needs only $220. The trade size is identical; the margin requirement differs by a factor of 16. Higher leverage frees up account equity for other trades, but it also means a smaller adverse move can wipe out your usable margin.

Regulatory Leverage Caps — Who Caps What

ESMA (EU) limits retail leverage to 1:30 for major forex pairs, 1:20 for minors and gold, and 1:10 for commodities and indices. The FCA (UK) and ASIC (Australia) impose nearly identical restrictions. Offshore brokers — regulated in the Cayman Islands, Vanuatu, or the British Virgin Islands — commonly offer 1:200 to 1:500. The trade-off is clear: higher leverage means less regulatory oversight and weaker investor protection.

Margin Calls and Stop-Outs — The Sequence

A margin call triggers when your equity drops below the used margin threshold — typically 100% of the margin requirement. The broker warns you to deposit funds or close positions. If equity continues falling to the stop-out level (usually 50% or 20% of required margin, depending on the broker), the platform automatically closes your weakest positions, starting with the largest loss, until equity recovers above the threshold.

Example: You hold a position with $1,000 used margin. Your equity drops to $500. At a 50% stop-out, the broker starts liquidating. You do not get a vote.

Why Lower Leverage Is Safer for Beginners

A 1:500 account lets a new trader open a standard lot with $220. A 30-pip move against them on EUR/USD loses $300 — more than the entire margin. The account is effectively blown in one trade. At 1:30, the same trader needs $3,667 in margin, which forces them to trade smaller sizes or fund the account properly. That forced discipline is the single strongest argument for choosing a regulated broker over a high-leverage offshore shop.

Position Sizing — The 1–2% Rule

Calculate lot size with three inputs: account equity, risk per trade (1–2%), and stop-loss distance in pips.

Formula: Lot size = (Account equity × Risk %) ÷ (Stop-loss in pips × Pip value per standard lot)

On a $10,000 account risking 1% ($100) with a 30-pip stop on EUR/USD (pip value = $10 per standard lot): $100 ÷ (30 × $10) = 0.33 lots. That is a mini-lot position. Stick to this math before you enter, not after you are underwater.

Deposits, Withdrawals, and the Fine Print on Your Money

Funding your account should be frictionless — getting your money back should be just as fast. The 2026 checklist puts equal weight on both directions of the pipeline.

Deposit Methods and Speed

Most brokers offer four main channels:

Bank wire — 1–3 business days. Free or low cost, but slow. Best for large sums.

Credit/debit card — Instant to a few hours. Some issuers flag forex deposits as cash advances; check your card terms.

E-wallets (Skrill, Neteller) — Near-instant. Fastest for withdrawals too, but some brokers charge a 1–2% fee on the deposit side.

Crypto (USDT, BTC) — Minutes to an hour, depending on network congestion. Increasingly common, but check whether the broker converts to fiat internally or holds the crypto — a detail buried in the fine print.

Withdrawal Speed and Friction

Fast deposit means little if withdrawal takes two weeks. The key question: does the broker allow withdrawals back to the original funding method? Regulators in the FCA and CySEC frameworks typically require this. If the broker insists on bank wire only, even for card depositors, that adds delay and cost.

Watch for these red flags in the terms of service:

Trading volume requirements before first withdrawal. Some brokers require you to trade a multiple of your deposit (e.g., 1 lot per $100 deposited) before you can request a payout. This is a liquidity trap, not a policy.

Withdrawal fees per request. $25–$50 on bank wires is common; anything above is a profit centre.

Minimum withdrawal amounts. $50–$100 is standard. Higher minimums ($200+) lock small accounts into accumulating risk they don't want.

Processing windows. Look for "within 24 hours" or "same business day." Avoid brokers that quote 5–10 business days before they even initiate the transfer.

Account Currencies and Conversion Costs

If your bank account is in EUR and the broker's base currency is USD, every deposit and withdrawal triggers a currency conversion — typically 2–3% each way. Open an account in your home currency if the broker offers it. Most regulated brokers support USD, EUR, and GBP base accounts; some add AUD, CHF, or JPY. Choosing the wrong base currency silently eats into your P&L on every transaction.

Dormant Account and Inactivity Fees

Check the fee schedule for inactivity after 90 or 180 days. A $10–$20 monthly dormant fee is common. If you trade seasonally, close the position and withdraw to zero before stepping away, or the broker will drain the balance itself.

Customer Support and Trader Resources That Actually Help

A broker with perfect spreads and zero commission means nothing when your withdrawal is stuck and nobody answers the phone. Support quality separates a professional trading environment from a frustrating one — and it is fully testable before you fund a live account.

Support Availability: 24/5 vs. 24/7

Forex markets run 24 hours a day, five days a week, so 24/5 support covers the full trading week. A broker offering 24/7 support adds weekend coverage — useful if you trade crypto CFDs or need help with platform issues before Monday's open. Test live chat response time during peak liquidity hours (London-New York overlap). Anything over two minutes is slow by current standards. Phone support should connect you to a human, not a voicemail tree, within three rings. Multilingual support matters if English is not your first language or you trade instruments tied to a specific region.

Educational Resources: Signal vs. Noise

Many brokers flood their sites with "analysis" that is really a soft sell for their own products. Filter for substance: daily market commentary that references actual economic data releases, webinars hosted by traders who show losing trades alongside winners, and trading guides that explain risk management before entry strategies. If every piece of content ends with a bonus offer or a "sign up now" button, it is marketing fluff, not education.

Demo Account Quality

An unlimited demo lets you test strategies without a clock running out. A 30-day demo forces a decision window that may not align with your learning curve. More important than duration is execution quality: does the demo fill orders at the same speed and slippage profile as the live environment? Some brokers use simulated liquidity that fills every trade instantly — creating an unrealistic edge that vanishes on a real account. Ask support directly whether demo fills match live execution conditions.

Local Presence Matters

A broker with an office in your time zone processes withdrawals faster, offers local bank transfer options, and understands the regulatory framework you actually live under. Regional payment methods — like POLi in Australia, iDEAL in the Netherlands, or PromptPay in Thailand — signal that the broker has invested in that market rather than treating it as an afterthought.

The Bottom Line for Your Checklist

Before depositing, send a test message through live chat at 2 AM your local time. Ask a specific question about withdrawal processing. If the answer takes longer than 24 hours, cross that broker off — even the best regulated forex broker is frustrating when you cannot get a straight answer about your own money.

Account Types and Minimum Deposit: Matching the Offer to Your Capital

Standard, Mini, and Micro Accounts — Lot Sizes and Risk Control

Brokers offer account tiers defined by the minimum lot size and the pip value per contract. A standard account trades in 100,000-unit lots — one pip on EUR/USD is worth $10. A mini account uses 10,000-unit lots ($1 per pip), and a micro account uses 1,000-unit lots ($0.10 per pip).

For a trader starting with $500, a standard lot on a 1% risk model means a 5-pip stop-loss is already $50 — 10% of the account. The same trade on a micro account costs $0.50 per pip, giving room for a wider, more realistic stop. Smaller lot increments let you scale position size gradually as equity grows, rather than jumping from 0.01 to 0.10 lots with no middle ground.

Minimum Deposit Ranges Across Broker Tiers

Minimum deposits vary widely by broker model:

ECN / Raw-Spread accounts: $0–$50. These target active traders who bring their own volume. Spreads are tight but commissions apply per lot.

Standard accounts: $200–$500. Spreads are wider, commissions are baked into the spread, and no minimum volume is required.

Prime / Pro accounts: $1,000–$10,000+. Reserved for high-volume or high-net-worth traders, often with dedicated account managers and lower per-lot commissions.

If you are starting small, look for a broker that offers micro or mini accounts with a deposit floor at or below $100. Avoid brokers that require $500+ minimums for an account that still only trades standard lots — that combination forces oversized risk from day one.

Islamic (Swap-Free) Accounts

Swap-free accounts comply with Sharia law by waiving overnight interest credits and debits on positions held past the rollover point. Most brokers offer them to Muslim traders who submit a declaration of faith. The catch: many brokers restrict swap-free accounts to a holding period of 7–14 days per trade, after which they either charge a flat administrative fee or close the position. Others limit the number of concurrent open trades. Always check the broker's swap-free policy in the terms and conditions — the "free" part applies only within those bounds.

Demo vs. Live — Execution, Slippage, and Psychology

A demo account uses delayed or simulated market data and fills orders at the quoted price with no requotes. A live account faces real liquidity gaps, slippage during news events, and variable spreads that widen when volatility spikes. The psychological difference is larger than most beginners expect: demo losses feel reversible, live losses affect your capital. Use the demo to test strategy logic and platform mechanics, then transition to a micro live account to experience real execution conditions with minimal financial risk.

What to Look for When Starting Small

If your starting capital is under $1,000, prioritise these features:

Low minimum deposit — $50 or less, so most of your capital stays in your trading account, not tied up in the deposit requirement

Micro or nano lots — position-size increments of 0.01 lots (1,000 units) or smaller

No inactivity fees — some brokers charge $10–$15 per month after 90 days of no trading, which eats a small account alive

A solid demo — at least 30 days of unlimited demo access so you can validate your approach before committing real money

FAQ

What is the most important factor when choosing a forex broker?

Regulation is the single most important factor. A broker licensed by a top-tier authority — the FCA (UK), CySEC (Cyprus), ASIC (Australia), or CFTC/NFA (US) — must meet strict capital adequacy, client segregation, and reporting standards. Without credible regulation, your funds have no independent protection. Check the regulator's register directly, not the broker's website, to confirm the license is active and covers the entity you are depositing with.

Can I trade forex with a small account — under $100?

Yes, many brokers now offer micro or cent accounts with no minimum deposit. A $50 account on a cent account means each standard lot is 1,000 units instead of 100,000, giving you position sizes as small as 0.01 micro lots. The tradeoff is that fixed costs — spreads and commissions — eat a larger percentage of a small balance. Stick to brokers offering raw spreads and low commissions to avoid losing 20% of your account to fees in the first week.

Are unregulated offshore brokers safe to use?

No, they carry significant risk. Offshore brokers operating without a recognised licence are not required to segregate client funds, submit to audits, or participate in any compensation scheme. If the broker becomes insolvent or simply disappears, you have no legal recourse. Some traders accept this risk for higher leverage or looser restrictions, but the safer path is a regulated broker that still offers competitive conditions — many do.

What is the difference between a Market Maker and an ECN broker?

A Market Maker takes the other side of your trade and may quote wider spreads or manipulate prices against you. An ECN (Electronic Communication Network) broker passes your order directly to liquidity providers and charges a transparent commission, typically $3–$7 per standard lot round-turn. ECN brokers generally offer tighter spreads and no conflict of interest, but require higher minimum deposits and may charge a monthly inactivity fee.

How long do broker withdrawals usually take?

Withdrawal times vary by method and broker. E-wallets (Skrill, Neteller) typically process within 24 hours. Credit/debit cards take 2–5 business days. Bank wire transfers are the slowest at 3–7 business days. Reputable brokers process withdrawal requests within one business day; the delay is on the payment provider side. Avoid brokers that charge excessive withdrawal fees or take longer than 10 business days — that is a red flag for liquidity or solvency problems.

អានបន្ត